With all the buzz about falling mortgage rates, the idea of rate increases feels like something out of an alternate universe. But here’s the truth: even when rates are trending downward, it’s never a straight shot. One week we may be talking about mortgage rates dropping and the next week could see them ticking upward.

This leads us to wonder: Where are fixed mortgage rates heading next?

Fixed Mortgage Rates: A Roller Coaster Without a Seatbelt

Trying to predict where fixed mortgage rates are heading is like trying to predict the weather six months out. Sure, it’s possible it could be correct, but it will almost certainly change.

The biggest wildcard? The ever-unpredictable policies (and social media posts) of U.S. President Donald Trump.

While the Bank of Canada is expected to continue to cut its rate this year, it’s certainly not guaranteed. US inflation shot up to 3.00% on Wednesday, February 12th. This resulted in US treasury yields surging, which brought Canadian bond yields along for the ride. As the yields play a large role in fixed mortgage rate pricing, we watch them closely. While today’s yield spike won’t immediately push fixed mortgage rates higher, if it continues then fixed mortgage rates would have no choice but to follow suit.

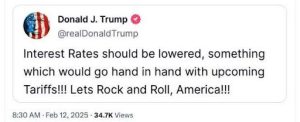

The Trump Factor: One Tweet Away from Chaos

Yes, the general expectation is that fixed mortgage rates will drop. But expecting something doesn’t make it true.

The problem is Trump’s unpredictability. Case in point: Right before the US inflation report was released; Trump posted the following on his platform Truth Social:

Cue every economist collectively banging their heads on their desks.

Seriously Trump?

Here’s the thing: tariffs drive inflation up. And as long as inflation remains a problem, the U.S. Federal Reserve isn’t cutting rates. In fact, after Wednesday’s inflation spike, rate cuts could be delayed even further.

Check out my recent blog on The Effect of Trump’s Tariffs on Canadian Mortgage Rates.

What About the Bank of Canada?

Even if the Bank of Canada continues with rate cuts, fixed mortgage rates have a mind of their own. Here’s a perfect example. In Q4 of 2024, the Bank of Canada cut rates by 1.00%—yet fixed mortgage rates increased by roughly 0.30%.

So, what’s next? Here’s what Canada’s big banks are predicting:

- CIBC: 0.75% in cuts by the end of Q2, then holding steady through 2026.

- RBC: 1.00% in cuts by end of Q3, no change in Q4.

- Scotiabank: 0.25% cut by end of Q1, no further changes through 2026.

- TD: 0.75% in cuts by end of Q4, then no more changes.

- BMO: 0.50% in cuts by end of Q3, then holding steady.

- National Bank: 0.75% in cuts by end of Q3, followed by a 0.50% hike by the end of 2026.

These are educated guesses at best—subject to change faster than a gas station’s price board.

What This Means for Variable Rate Mortgages

If the above forecasts hold true, then variable rate mortgages could be a solid choice. That is, if you can stomach the uncertainty. It also has to be understood and accepted that it’s likely that the Bank of Canda will increase its rate at some point over the mortgage term.

National Bank is already forecasting 0.50% in hikes by the end of next year. That’s still pretty far out and the forecast will certainly change. If the thought of rate hikes keep you up at night, then a variable rate mortgage may not be worth the stress.

Final Thoughts

Trying to predict mortgage rates with Trump in office is like playing darts while blindfolded in a windstorm. Could you hit the bullseye? Maybe. But it’s mostly luck.

Even the Bank of Canada doesn’t know what’s coming next. The U.S. has made it clear they’re in no rush to cut rates. If inflation stays stubborn, they may even increase rates instead. Let’s hope that doesn’t happen—but let’s also be realistic.

Bottom line? Anything can happen. And in this economic climate, “expect the unexpected” should be every borrower’s new motto.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment